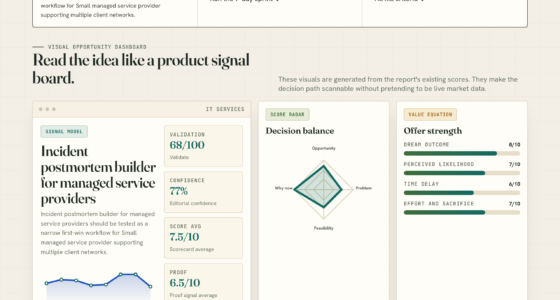

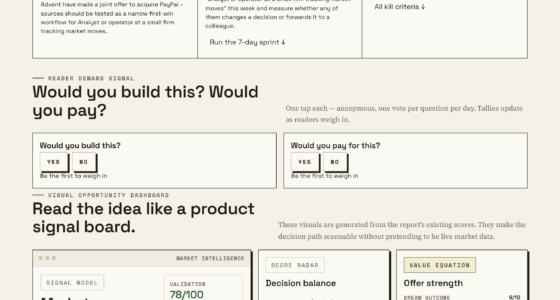

📊 Full opportunity report: The gigawatt gap. Why China is structurally positioned for AI power and the US is engineering around its grid. on ThorstenMeyerAI.com — validation score, market gap, and execution plan.

TL;DR

China’s centralized infrastructure and renewable buildout enable it to deploy lower-performance chips at gigawatt scale, closing the AI power gap with the US. The US faces constraints at the physical power delivery layer, risking a structural ceiling in AI deployment.

China has achieved a significant structural advantage in AI infrastructure by deploying gigawatt-scale power capacity, enabling it to compensate for lower-performance chips compared to the US. This shift challenges US dominance in AI deployment, which is constrained by grid and permitting bottlenecks at the physical power delivery layer.

While US AI chips and models remain ahead in raw silicon performance, China’s strategy focuses on substituting power throughput for chip performance. The Chinese government’s Eastern Data Western Compute initiative routes eastern AI demand to western renewable energy hubs through extensive ultra-high-voltage (UHV) transmission projects totaling over 40,000 kilometers, with a capacity of 340 GW. In 2025, China added over 430 GW of wind and solar capacity, surpassing US renewable additions.

Chinese AI chips, such as Huawei’s Ascend 910C, perform at roughly 60% of NVIDIA’s H100 inference levels and lack native FP8/FP4 support. However, system-level asymmetry favors China because it can deploy more chips powered by abundant renewable energy, effectively closing the system-level gap. The US, in contrast, faces regulatory and transmission constraints that limit the physical deployment of infrastructure, despite having more advanced chips and models.

This structural difference is rooted in the US’s federal fragmentation, which complicates permitting and siting of large-scale power infrastructure, versus China’s centralized planning and state-controlled grid, which facilitates massive renewable buildout and transmission projects. Consequently, China’s approach is less about chip performance and more about power throughput, enabling large-scale AI deployment despite lower chip efficiency.

The gigawatt gap.

Why China is structurally

positioned for AI power

and the US is engineering

around its grid.

power capacity end 2025

5-year average wait

45 projects · 340 GW capacity

vs. H100 · compensated by watts

interconnection queue

installed capacity

built by end-2024

on-site generation

DY 2024-25 → 2026-27

solar additions 2025

generation capacity

installed base

of capacity

add ratio

2025 alone

capacity end 2025

installed capacity

of capacity

Low watts

grid + transmission capacity

More watts

chip performance / FP precision

The US has perf-per-watt advantage. China has watts-without-bound advantage. These are asymmetric substitutes — not the same axis. When the perf-per-watt side is bounded by grid capacity and the watts-without-bound side is bounded by chip performance, the binding constraint differs.Thorsten Meyer · The Gigawatt Gap · Energy & Infrastructure 01

Implications of Power Infrastructure for Global AI Leadership

This development indicates that AI infrastructure at the frontier is increasingly governed by physical power delivery capacity rather than silicon performance alone. China’s ability to leverage its centralized planning and renewable energy scale could enable it to deploy AI at a larger scale than the US, potentially shifting the global leadership in AI deployment. For the US, overcoming grid and permitting bottlenecks is now critical to maintaining its technological edge, as the power layer becomes a new frontier for strategic competition.

ARESGAME AGV Series 500W Power Supply, 80 Plus Bronze Certified, Non Modular Power Supply, 5 Year Warranty

- Power Output: 500W continuous power supply

- Certification: 80 Plus Bronze certified for efficiency

- Warranty: 5-year warranty included

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

The Shift Toward Gigawatt-Scale AI Data Centers

Until recently, AI data centers operated at megawatt to low gigawatt capacities, with the US leading in chip performance and infrastructure. However, recent developments show that frontier AI sites now require 1–2 GW of power, with some full-scale campuses reaching 5 GW. The US has responded with workaround solutions, including off-grid gas turbines, nuclear contracts, and regulatory arbitrage, to bypass grid constraints. Meanwhile, China’s centralized planning and extensive renewable buildout have created a different infrastructure paradigm, allowing deployment of lower-performance chips across vast power networks.

China’s strategy is underpinned by the Eastern Data Western Compute initiative, which connects renewable energy hubs to AI demand centers via ultra-high-voltage transmission, enabling large-scale AI deployment independent of local grid constraints. This approach contrasts with the US’s fragmented grid, which hampers large-scale, siting, and permitting processes, thus constraining AI infrastructure growth at the physical power layer.

“The gigawatt-scale capacity requirements of frontier AI deployments are reshaping the infrastructure landscape, with China leveraging its centralized planning to deploy massive renewable energy and transmission infrastructure, while the US faces regulatory and grid bottlenecks. See the full analysis for more details.”

— Thorsten Meyer

NooElec SMA DC Block in-Line 50 Ohm 50kHz-8GHz Connector Blocks DC Voltage from Your Radio or RF Test Equipment. Ultra-Low Insertion Loss (<0.3dB to 6GHz) and 2 Watts Maximum Power

- Frequency Range: 50kHz to 8GHz

- Voltage Blocking: Up to 50V

- Power Handling: Maximum 2W

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Uncertainties About Future Efficiency Gains and Policy Changes

It remains unclear whether the US can close the power throughput gap through efficiency improvements in chips, racks, and models, or if regulatory and structural constraints will impose a sustained ceiling. The impact of potential policy reforms, technological advances, and grid modernization efforts on this dynamic is still uncertain. Additionally, the extent to which China’s reliance on lower-performance chips will continue to suffice as AI models evolve remains an open question.

L6-50P 50 Ampere Rack Mounted PDU Power Socket with 8-Position C13 Socket Output Circuit Breaker Protection, Aluminum Alloy Shell 6-Foot 8AWG Cable (C13-08-S)

- Maximum Load: 50 Ampere capacity

- Power Cord Length: 6-foot 8AWG cable

- Monitoring Features: Voltage ammeter included

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Next Steps in AI Infrastructure Competition

Over the next 24 months, developments will focus on whether the US can reform permitting processes, expand grid capacity, and improve power infrastructure to match China’s gigawatt-scale deployments. Simultaneously, China’s continued renewable buildout and transmission expansion will be key factors. Monitoring policy changes, technological improvements, and deployment scales will determine whether the power layer becomes a new bottleneck or a strategic advantage.

wind turbine generator 10KW

- Power Capacity: 10KW wind turbine generator

As an affiliate, we earn on qualifying purchases.

As an affiliate, we earn on qualifying purchases.

Key Questions

Why is power infrastructure now critical for AI deployment?

Because frontier AI data centers require gigawatt-scale power capacity, and the physical infrastructure needed to deliver electricity to silicon is the limiting factor, not the chips themselves.

How does China’s approach differ from the US in deploying AI infrastructure?

China leverages centralized planning, large renewable energy buildout, and extensive ultra-high-voltage transmission to deploy lower-performance chips across vast power networks, bypassing local grid constraints. The US relies on fragmented infrastructure, regulatory arbitrage, and off-grid solutions.

What are the risks for the US if it cannot overcome grid and permitting constraints?

The US could face a structural ceiling in AI deployment at the physical power layer, potentially ceding global leadership in AI scale and capability to China, which is building its infrastructure differently.

Will efficiency improvements in chips close the gigawatt gap?

It is uncertain. While chip efficiency gains continue, the fundamental structural constraints on physical power delivery may persist, making infrastructure the key battleground.

What role will policy reforms play in this competition?

Reforms that simplify permitting, expand grid capacity, and facilitate large-scale infrastructure projects could help the US mitigate the physical constraints and maintain its AI leadership.

Source: ThorstenMeyerAI.com